Cibil Credit Report

Get Lifetime Free Credit Score & Report

Your Personal Information is 100% secured with us. We do not share your data with any third party.

What is Credit Score?

A credit score is a 3-digit numeric summary of your credit history that represents your past credit behavior and how well you have managed your credit products, like Personal Loan credit cards, home loans, business loans, auto loans, overdrafts, credit lines, etc. Credit score, which is also commonly referred to as CIBIL score is primarily a measure of your ability to borrow from banks and NBFCs and financial institutions. CIBIL score is calculated and generated based on the consumer’s credit information provided by the lenders to credit bureaus on a monthly basis.

Simply put, your credit score shows lenders whether you are a reliable borrower with minimum risk or a risky one, as well as the likelihood of you repaying a new loan in time. When you apply for any type of loan or a credit card, the lender requests a credit report check from the credit bureau to know your repayment capability and creditworthiness.

CIBIL score ranges from 300-900 in which the higher your credit score, the more likely lenders are to approve you for new credit. Usually, a credit score of 760 and above is considered a standard benchmark and preferred by lenders for loan or credit card approval. For a few banks/NBFCs, even a credit score of 700+ is also considered for credit card approvals.

If you miss EMI of your loans or your credit card bills on time, your score is negatively impacted. On the other hand, if you have been disciplined with the repayments of your EMIs and credit card bills, and have not displayed any credit-hungry behavior by frequently applying for credit, your credit score shall tend to increase.

Benefits of a Credit Score

Your credit score is one of the first things that a lender bank or NBFC will check while evaluating your loan application. In case your credit score is low, then try to improve it at the earliest or else the lender might reject the application without even considering it further.

If your credit score is high, the lender will look into other details to determine, such as your creditworthiness and repayment capacity. Thus, a good credit score increases the chances of your loan application’s approved and helps in availing funds at ease..

However, your credit score is not the only factor considered for a person’s ability to get a new credit. Lenders also consider your income, repayment capacity, debt-to-income ratio, employment history, profession, etc. before approving or rejecting your loan or credit card application.

A good CIBIL score would not only help you access credit, but it may also help reduce your interest outgo for a loan. Many banks/NBFCs offer preferential low-interest rates to applicants with a good credit score and repayment history.

What is a Good Credit Score?

Today, most lenders consider a credit score of 760 and above from CIBIL or any credit bureau as a good credit score. Getting the loan or credit card application approved becomes relatively easier if you have and maintain a CIBIL score of 760 or above and as close to 900. It is possible to have a CIBIL score of 760 or above and have a credit score from another bureau below 700 at the same time. Hence, you must keep a tab on credit scores from multiple bureaus. It is advisable to check your credit score once every month.

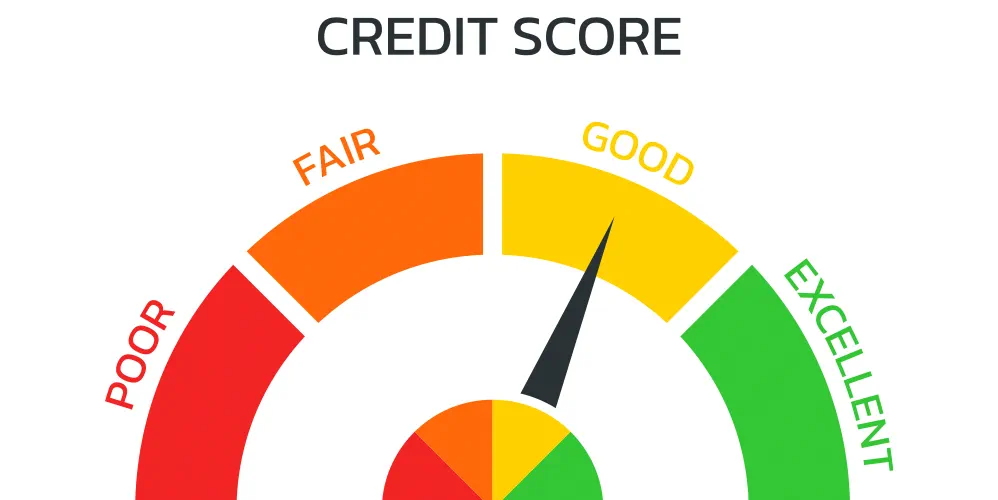

Credit Score Range and Meaning

Let us have a look at most lenders and bureaus consider while evaluating your credit applications:

| Score Band | Category | Meaning |

| <300 | No Score/No History | It means you have never taken a loan or credit card and have no credit history. For the best offers on loans and credit cards in the future, you should start building your credit score. |

| 300-550 | Very Low Credit Score | Your credit history is damaged. However, with awareness and discipline, you can strengthen your credit score. Check your credit report thoroughly to determine why your credit score is low and take action. |

| 551-620 | Low Credit Score | You might not have shown good credit behavior that has damaged your credit history. You need to take immediate measures to improve your score to become eligible for credit in the future. |

| 621-700 | Fair Credit Score | You are not far from a strong credit score. To be eligible for the best offers, you should work on improving your score. |

| 701-759 | Good Credit Score | You have been responsible with credit and have displayed good credit behavior. Most banks and NBFCs would be happy to offer you credit. |

| 760+ | Excellent Credit Score | Your track record with credit is superb! With this score, you would meet the eligibility criteria of most banks and NBFCs and are likely to get the best offers. |

Please Note: The credit score range mentioned above is only indicative and may vary from lender to lender and bureau to bureau.

How a Credit Score is Calculated?

Your credit score depends on a lot of factors that a credit bureau or Credit Information Companies (CICs) takes into consideration while calculating your CIBIL score. These factors depict your past credit behavior and are reported to banks and NBFCs, every time you apply for a fresh credit product.

5 Factors that Affect your Credit Score

Some of the key factors that influence your credit score are:

1. Loan Repayment History: Timely payments can boost your credit score and help in improving it significantly. Defaulting on your EMIs or making late payments negatively affects your CIBIL score. Your loan repayment history has a high impact on your CIBIL score calculation.

2. Duration of Credit History: The duration or age of your credit history also affects your credit score. If you have used credit cards/loans for a long period and made timely payments on them, then it’s a sign of disciplined credit behavior. It has a medium impact on your credit score.

3. Number of Hard Inquiries: Every time you apply for a new credit product, the lender inquires about your credit score. Such inquiries by lenders and financial institutions are known as hard inquiries. Too many hard inquiries may negatively affect your credit score as it shows you to be credit-hungry. Multiple hard inquiries at the same time may have a considerable short-term impact on your credit score. However, if you check or download your credit report, it is considered a soft Inquiry that has no impact on your credit score.

4. Credit Utilization: The ratio of the credit amount you spend to the credit amount available to you is known as the credit utilization ratio. It is recommended to keep your CUR to less than 30% of your available credit limit, though even a higher CUR barely has an impact on your credit score as long as you pay your credit card bill on time. However, maxing out the limit on your credit card frequently may indicate a high dependency on credit, which may negatively impact your credit score.

5. Credit Mix: If you have taken different kinds of loans like personal, auto or home loans and have responsibly paid them back, it shows your ability to handle different kinds of credit. Building a good credit mix over time has a positive impact on your credit profile. Also, if you have taken too many unsecured loans like personal loans, it shows you are credit-hungry and excessively dependent on credit. This may have an impact on your credit score, but if your repayment record is strong, it’s unlikely to be anything significant.

Do note that having too many active loans at the same time can also lead to a high “EMI to NMI ratio”, which can lower your chances of getting more credit. However, credit mix has a low impact on your credit score and it’s unlikely that a lender will reject your application just because you do not have an optimum mix of credit products.

Benefits of High Credit Score

Though credit score is not the only thing lenders check while considering a loan or credit card application, it is arguably one of the most important. comes with several benefits that include:

- Greater chances of your loan applications being approved, as a high CIBIL score indicates higher creditworthiness and lower risk for the lender

- You are more likely to receive report same day

- You can get easy and quick approval for your loan and credit card applications

- Access to pre-approved loans based on your eligibility

- You can avail higher limits on your credit cards

- Discount on processing fees and other charges

Impact of CIBIL Score on your Loan & Credit Card Eligibility

Your credit score is an important factor when assessing your loan or credit card eligibility. Where a good credit score increases your chances of availing the loan or credit card on better terms, a poor credit score can reduce your chances of credit approval significantly.

Generally, most lenders and credit card providers consider a CIBIL score of 760 and above as good enough to approve most applications considering other parameters are fulfilled.

However, the closer the score to 900, the higher the chances of credit approval. A higher score empowers you to avail a loan at relatively lower rates and better loan terms.

A poor credit score due to indiscipline in repayments and loan defaults can make it difficult to get your loan or credit card applications approved in future. The more severe the issue in your credit report, the poorer your credit score and the lower the chances of your credit approval.

When your score is low, you should focus on improving it first. Apply for a credit product only when your score becomes healthy.

Credit Bureaus in India

Transunion Limited (Formerly known as Credit Information Bureau (India) Limited) is a credit bureau that generates, maintains, and calculates your CIBIL score. While TransUnion CIBIL is the oldest, three other credit bureaus in India offer credit report services, Each credit bureau calculates your credit score independently based on the credit information that is provided to them by banks/NBFCs regularly. Each credit bureau has its model or algorithm for calculating your credit score; hence, your score from each credit bureau shall vary.

At Policybulls.com, you can check your credit score online for FREE and download customised credit reports. We have a partnership with all four leading credit bureaus, including CIBIL, that enables you to check, track and build your credit score at absolutely zero cost.

Please note that checking your credit report once or multiple times does not have any impact on your score and it takes just a few minutes.

Credit Score for NRIs

People having NRI PAN cards, and who have availed credit facilities in the past, get a credit score assigned to them. Its calculation is based on the same algorithm that is used to calculate the credit score for resident borrowers. NRIs, who intend to avail credit facilities in future, can stay updated with their score and work to improve it, if required. A credit score of 750 or above in India may help them in getting their loan applications approved without much difficulty if other criteria are fulfilled.

It is worth noting that credit scores are not transferrable between countries. For example, if you have an Experian credit score of 750 in India, you may have a different credit score in the USA. The scoring is based on the credit behaviour in a particular country and not on collective credit behaviour in all countries. So, if you have a good credit score in a particular country, you may still have to work on improving your credit score in India.

6 Reasons Why you Have a Low Credit Score

There can be several reasons. Some of the main factors that can lower your credit score are:

- Missed or late payments of credit cards and loan EMIs

- Maxing out your credit limit or having a high credit utilization ratio, regularly

- Errors in your credit report can also lower your score significantly

- Frequent or multiple hard inquiries for credit can also damage your credit score

- Closing the oldest credit account if other credit accounts are relatively new (It reduces the age of credit history)

- Settling the loan or credit card account instead of paying it in full and closing the account

How to Improve Credit Score?

A low credit score can make it difficult for you to get your loan or credit card applications approved. You can take the following steps

- Start paying your loan EMIs and credit card bills on time. Do not miss payments under any circumstances.

- Reduce your excessive dependency on credit and try to reduce your credit utilization ratio, especially if you max out your credit card limit regularly

- In case of errors in your credit report, get it rectified at the earliest from the credit bureau. For this, you should check your credit score online regularly through Policybulls and if there’s a fall, do check the report for errors.

- Avoid applying for multiple loans or credit cards very frequently. It is advisable to wait for six months to avail the latest credit instrument before you apply for credit again.

- Avoid closing your oldest credit card. A longer credit history helps lenders make credit-related decisions with more confidence.

- Keep a good mix of secured (home loan, car loan, etc.) and unsecured credit (personal loan, credit card, etc.) in your profile.

- Seek expert advice from Policybulls Credit Advisory Services to improve your credit score significantly.

Why Check your CIBIL Score from Policybulls ?

Apart from the fact that Policybulls offers CIBIL score for FREE with monthly updates, you can also check, monitor, and compare your credit scores from other credit bureaus like Experian, CRIF High Mark, and Equifax. Policybulls helps you check, track, and build your score by enabling you to:

- Check your credit score seamlessly: Through Policybulls.com (web & app), you can check and compare your credit score from multiple bureaus, including CIBIL, instantly and for absolutely free. Since it’s a digital instant process, you can access your latest credit score in a few seconds from anywhere, anytime for free.

- Get customized offers: Those with healthy credit profiles can also check and avail of the best pre-approved loan and credit card offers from India’s top banks and NBFCs. These offers have no/minimum documentation and usually have instant disbursals and issuance. Through Policybulls unique

- ‘Chances of Approval’ feature: You will be matched with the most-suited lender and offer for personal loans, based on your CIBIL score along with other eligibility factors. This will help you apply for the right offer from the right lender, minimizing the chances of rejection of your loan application.

- Build your credit score: To improve access to formal credit, Policybulls also offers a personalized that helps customers understand their credit report and improve their CIBIL score or credit score. Policybulls also provides an exclusive credit health report, with deep analysis